During the pandemic, the stock prices almost doubled, but their trends have recently declined. One of the reasons for that might be the interest rates. To examine this, we will take a consideration ARK Innovation ETF (ARKK), which is a long-term growth capital by investing mostly in tech companies.

First, we will create our datasets. The interest rates we are going to use are long-term interest rates that induced investment, so which is related to economic growth.

library(tidyverse)

library(tidyquant)

library(sysfonts)

library(showtext)

library(gghighlight)

library(tidymodels)

library(timetk)

library(modeltime)

library(tsibble)

library(lubridate)

library(fable)

library(ggtext)

library(scales)

#Building monthly dataset from daily prices

arkk_monthly <-

tq_get("ARKK") %>%

mutate(month = floor_date(date, "month"),

close = round(close, 2)) %>%

group_by(month) %>%

slice_max(date) %>%

select(date, price = close, volume)

#US long-term interest rates

interest_df <-

read_csv("https://raw.githubusercontent.com/mesdi/blog/main/interest.csv") %>%

#converting string to date format

mutate(date = parse_date(date, "%Y-%m"))

#Combining the two datasets

df <-

arkk_monthly %>%

left_join(interest_df, by = c("month"="date")) %>%

#converts date to the given string format

mutate(month = format(month, "%Y %b")) %>%

#converts string to the yearmonth object

mutate(month = yearmonth(month)) %>%

ungroup() %>%

select(-country) %>%

na.omit()

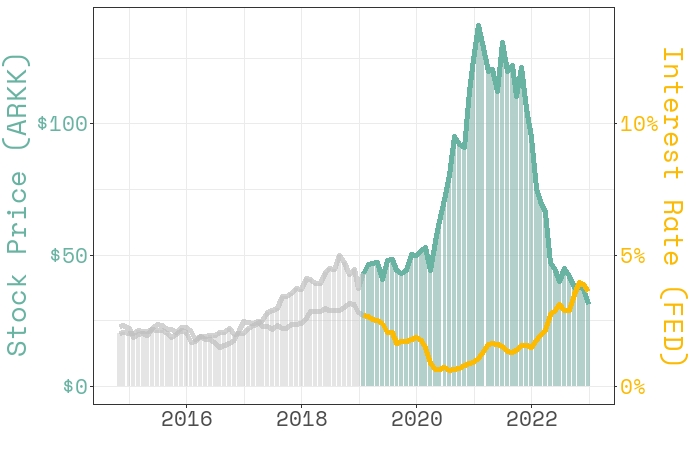

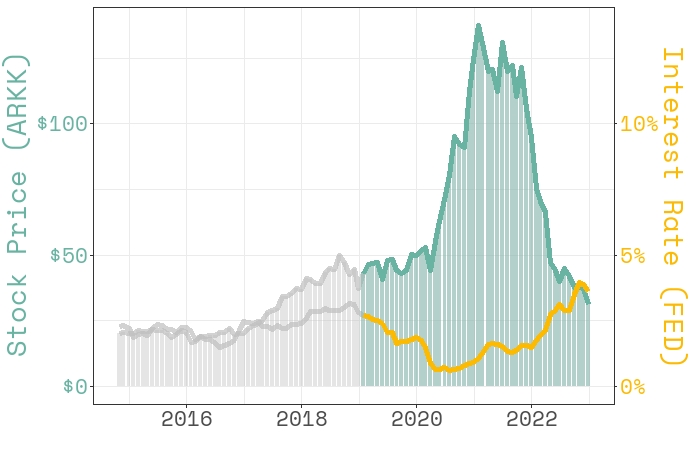

Now, we will take a look at how the stock prices of ARKK and long-term interest rates have gone along together.

#Comparing stock prices and interest rates

#adding google font

font_add_google(name = "Space Mono", family = "Mono")

showtext_auto()

df %>%

ggplot(aes(date))+

geom_bar(aes(y=price),

stat = "identity",

fill = "#69b3a2",

color= NA,

alpha = .4)+

geom_line(aes(y = price),

color= "#69b3a2",

size =2)+

geom_line(aes(y = interest*10), size =2, color = "#fcba03") +

#highlights the area after 2019

gghighlight(year(date) >= 2019)+

scale_y_continuous(

#Main axis

labels = scales::label_dollar(),

name = "Stock Price (ARKK)",

#Add a second axis

sec.axis = sec_axis(~./10,

labels = scales::label_number(suffix = "%"),

name="Interest Rate (FED)")

) +

xlab("")+

theme_bw(base_family = "Mono") +

theme(

text = element_text(size = 20),

axis.title.y = element_text(color = "#69b3a2"),

axis.title.y.right = element_text(color = "#fcba03"),

axis.text.y = element_text(color = "#69b3a2"),

axis.text.y.right = element_text(color = "#fcba03")

)

When we look at it, especially from 2019, we can clearly see the reverse relation between stock prices and interest rates.

Based on the above inference, we will model stock prices with interest rates. To do that, we will use boosted ARIMA regression model.

#Building train and test set

df_split <- time_series_split(data = df,

assess = "2 years",

cumulative = TRUE)

df_train <- training(df_split)

df_test <- testing(df_split)

#Modeling

#Preprocessing

df_rec <-

recipe(price ~ interest + date, df_train) %>%

step_fourier(date, period = 12, K = 6)

#Model specification

df_spec <-

arima_boost(

# XGBoost Args

tree_depth = 6,

learn_rate = 0.1) %>%

set_engine(engine = "auto_arima_xgboost")

#Worlflow and fitting

workflow_df <-

workflow() %>%

add_recipe(df_rec) %>%

add_model(df_spec)

set.seed(12345)

workflow_df_fit <-

workflow_df %>%

fit(data = df_train)

#Model and calibration table

model_table <- modeltime_table(workflow_df_fit)

df_calibration <-

model_table %>%

modeltime_calibrate(df_test)

#Accuracy

df_calibration %>%

modeltime_accuracy() %>%

select(rsq)

# A tibble: 1 x 1

# rsq

# <dbl>

#1 0.913

The high accuracy rate encourages us to proceed with that model. Now, we will forecast stock prices for the next 12 months. But first, we must build a dataset consisting of future values of predictors. We will use the automated stepwise ARIMA model for the interest rate variable.

#Future dataset for the next 12 months

date <-

df %>%

as_tsibble(index= month) %>%

new_data(12) %>%

mutate(month = as.Date(month),

date = ceiling_date(month, "month")-1) %>%

as_tibble() %>%

select(date)

interest <-

df %>%

as_tsibble(index = month) %>%

model(ARIMA(interest)) %>%

forecast(h = 12) %>%

as_tibble() %>%

select(interest = .mean)

df_future <-

date %>%

bind_cols(interest)

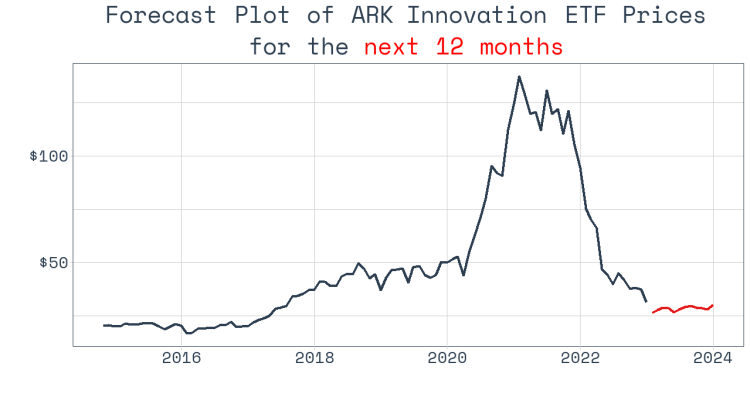

Finally, we refit the model on the whole dataset and draw the forecasting plot.

#Forecasting the next 12 months

df_calibration %>%

modeltime_refit(df) %>%

modeltime_forecast(new_data = df_future,

actual_data = df) %>%

plot_modeltime_forecast(.interactive = FALSE,

.legend_show = FALSE,

.conf_interval_show = FALSE,

.line_size = 1,

.title = "Forecast Plot of ARK Innovation ETF Prices for the <span style = 'color:red;'>next 12 months</span>")+

scale_y_continuous(labels = scales::label_dollar())+

theme(text = element_text(size = 20, family = "Mono"),

plot.title = ggtext::element_markdown(hjust = 0.5))

It looks like the prices will remain far below $50 in the coming year.

Leave a comment