Skip to content

Search

Home

About

Contact

Tag:

arima

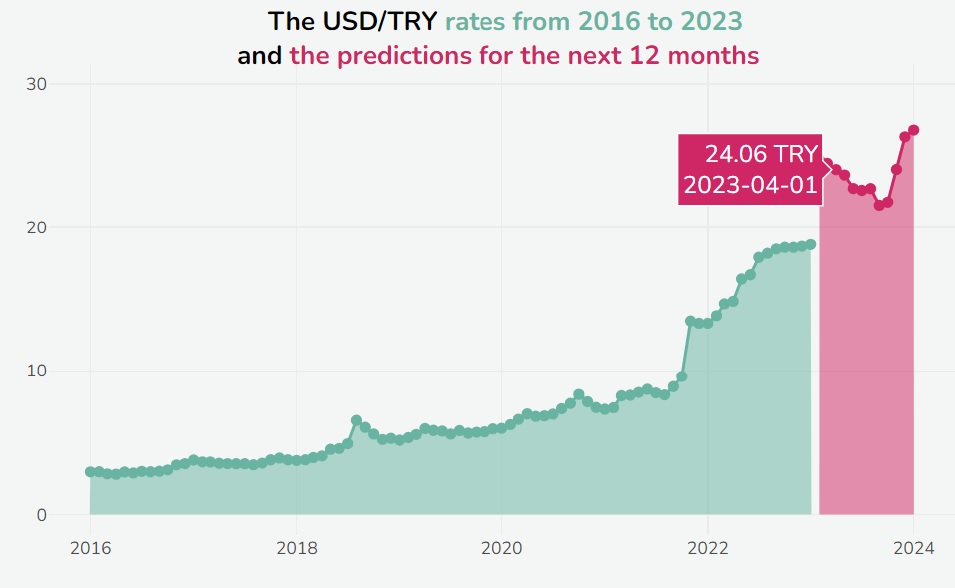

Predicting the Real USD/TRY Rates with MARS

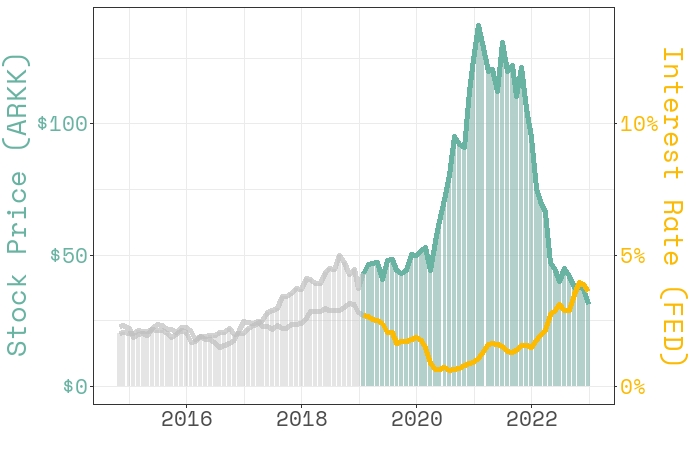

The Falling of ARK Innovation ETF: Forecasting with Boosted ARIMA Regression Model

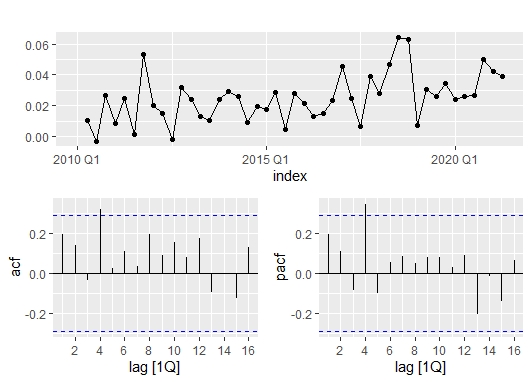

Dynamic Regression with ARIMA Errors: The Students on the Streets

Forecasting with ARIMA from {fable}: The Election is Coming for Turkey?

Next Page

Subscribe

Subscribed

DataGeeek

Join 59 other subscribers

Sign me up

Already have a WordPress.com account?

Log in now.

DataGeeek

Subscribe

Subscribed

Sign up

Log in

Report this content

View site in Reader

Manage subscriptions

Collapse this bar