-

Continue reading →: Analyzing Financial Trends: Kalman Filtering for Gold vs Bitcoin

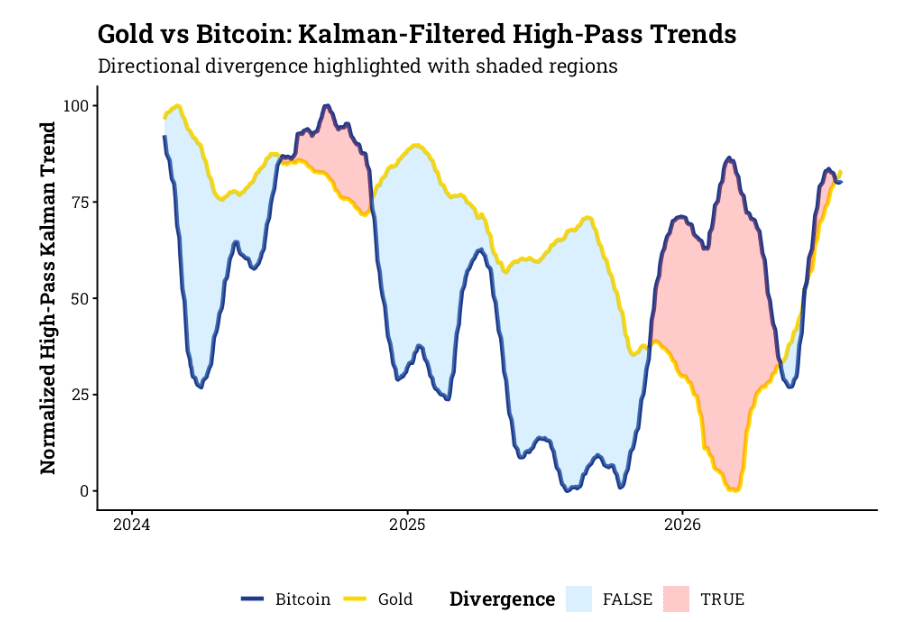

Continue reading →: Analyzing Financial Trends: Kalman Filtering for Gold vs BitcoinIn their paper “A Synchronized Multi‑IMU Wearable System for Tracking of Joint‑Angles in Sports Motion Analysis” (arXiv:2607.26027v1), Samarasekera and colleagues set out to solve a very practical problem: how to reliably measure joint angles in dynamic sports movements using wearable IMUs. Their goal was to design a synchronized pipeline that…

-

Continue reading →: Understanding Tail Analysis in Financial Markets

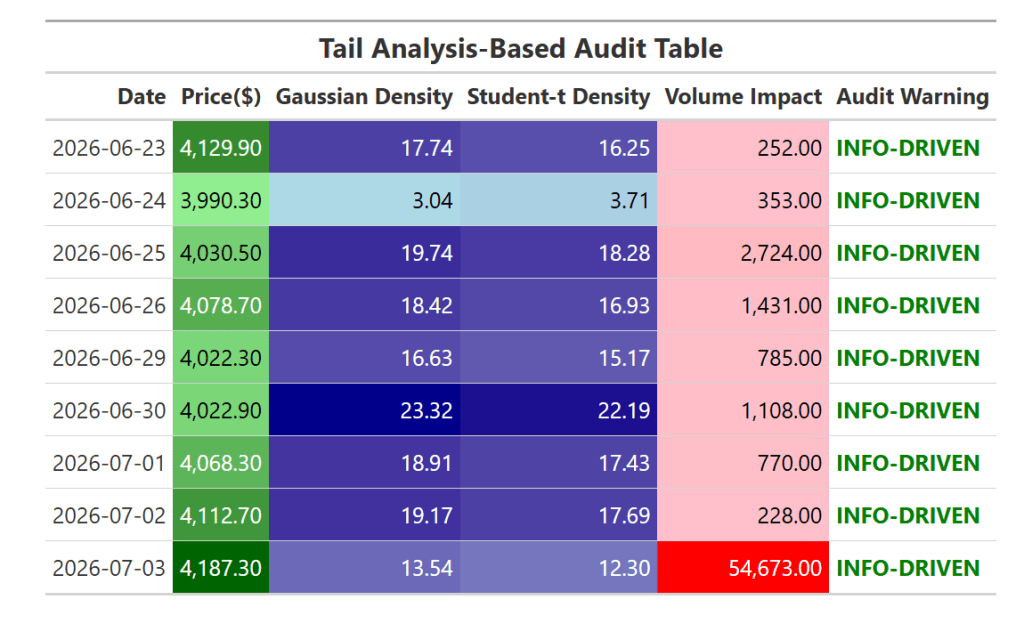

Continue reading →: Understanding Tail Analysis in Financial MarketsIn financial markets, distinguishing between information-driven movements and liquidity-driven shocks is critical. The reference study we based our work on highlights the importance of tail analysis: comparing Gaussian (thin-tailed) and Student‑t (fat-tailed) distributions to understand whether price changes are more likely to reflect genuine information or temporary liquidity imbalances. Financial…

-

Continue reading →: Auditing LLM Trading: Bridging Theory and Market Reality with the GT table in R

Continue reading →: Auditing LLM Trading: Bridging Theory and Market Reality with the GT table in RIntroduction: The Laboratorial Illusion In quantitative finance, Large Language Model (LLM) multi-agent systems are frequently celebrated for their theoretical intelligence. Financial data scientists spend months refining prompt semantics, building complex reasoning frameworks, and engineering multi-turn debate loops between specialized agent nodes. On paper—and within simulated environments—these networks demonstrate flawless predictive…

-

Continue reading →: A Multi-Agent DDQN Strategic Audit Engine for Silver Markets using Keras/TensorFlow

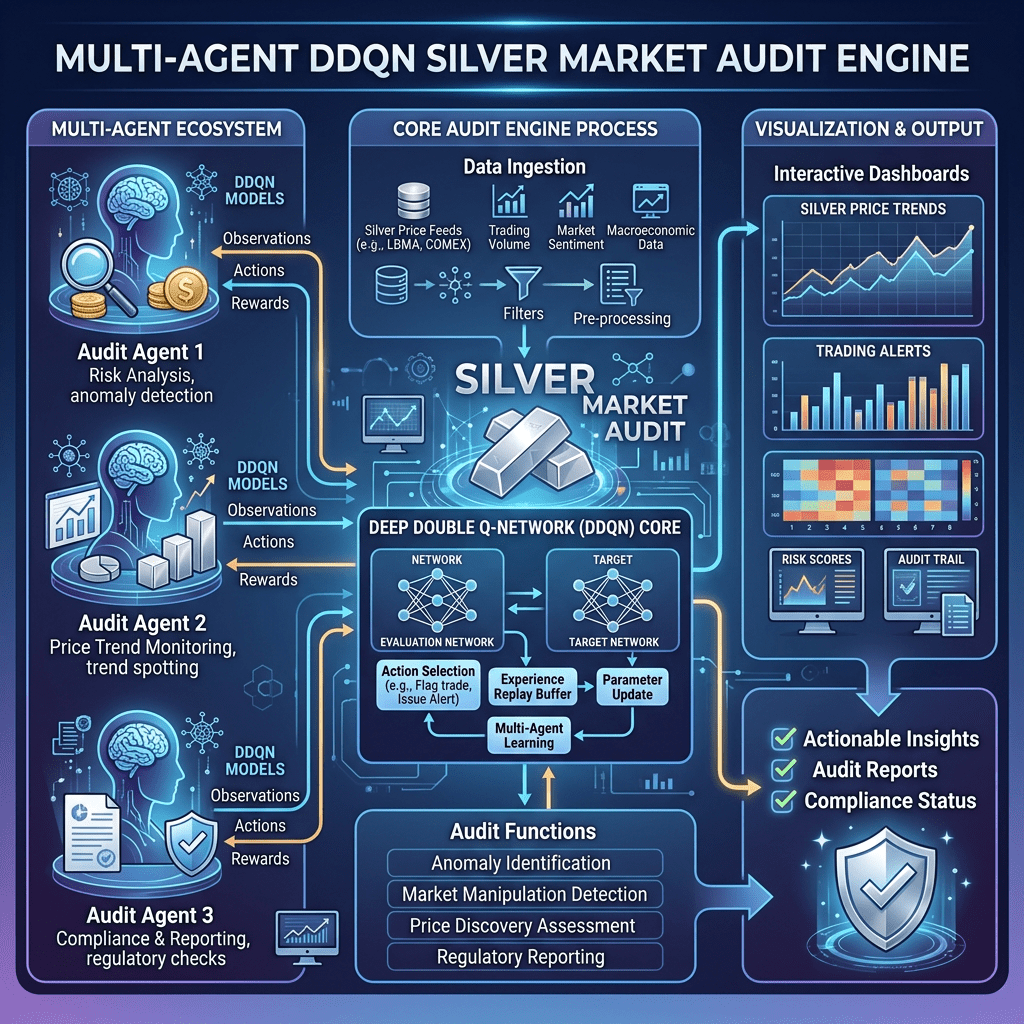

Continue reading →: A Multi-Agent DDQN Strategic Audit Engine for Silver Markets using Keras/TensorFlow1. Introduction & Theoretical Framework In modern electronic trading markets, algorithmic execution engines drive the vast majority of institutional order flows. Evaluating whether these independent, learning-driven trading algorithms behave competitively or tacitly coordinate has become a critical challenge for quantitative compliance, market microstructure design, and risk management. This technical article…

Hello,

I’m Selcuk Disci

The DataGeeek focuses on machine learning, deep learning, and Generative AI in data science using financial data for educational and informational purposes.

Let’s connect

Join the fun!

Stay updated with our latest tutorials and ideas by joining our newsletter.