Skip to content

Search

Home

About

Contact

Tag:

xgboost

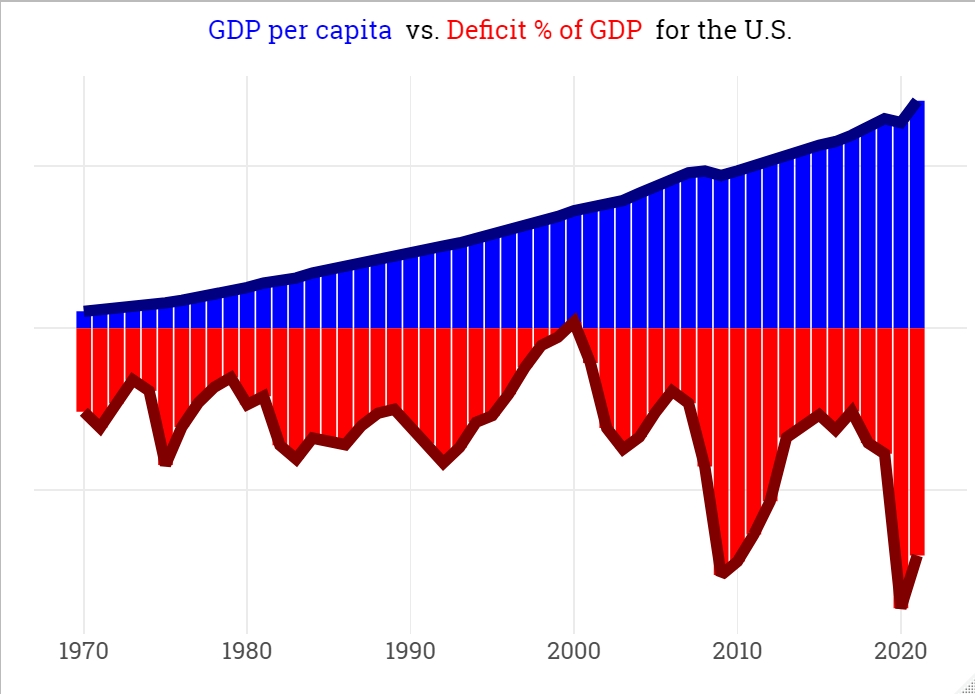

Impact of Budget Deficits on Treasury Yields with XGBoost

Explanatory Analysis of the XGBoost Model for Budget Deficits of U.S.

Dynamic Regression (ARIMA) vs. XGBoost

Time Series Forecasting with XGBoost and Feature Importance

Subscribe

Subscribed

DataGeeek

Join 59 other subscribers

Sign me up

Already have a WordPress.com account?

Log in now.

DataGeeek

Subscribe

Subscribed

Sign up

Log in

Report this content

View site in Reader

Manage subscriptions

Collapse this bar