Skip to content

Search

Home

About

Contact

Tag:

dynamic regression with ARIMA errors

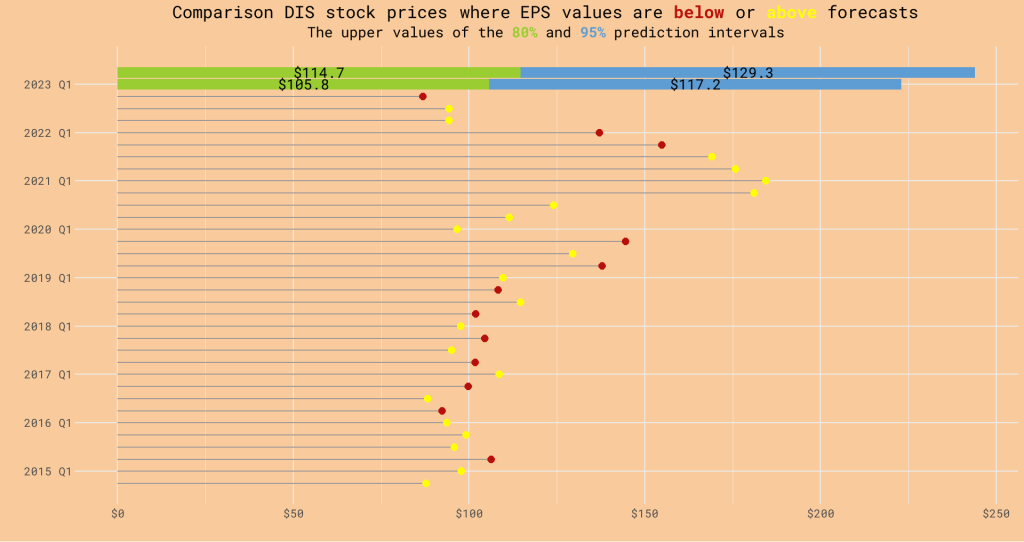

Forecasting Disney Stock Prices as the Latest Earnings Beat Estimates

Lagged Predictors in Regression Models and Improving by Bootstrapping and Bagging

Dynamic Regression with ARIMA Errors: The Students on the Streets

Dynamic Regression (ARIMA) vs. XGBoost

Subscribe

Subscribed

DataGeeek

Join 59 other subscribers

Sign me up

Already have a WordPress.com account?

Log in now.

DataGeeek

Subscribe

Subscribed

Sign up

Log in

Report this content

View site in Reader

Manage subscriptions

Collapse this bar